Financial freedom ka sapna har investor dekhta hai, lekin Mutual Fund Investment ki sahi samajh na hone ke karan log deri kar dete hain. Wealth creation ki duniya mein ek term hai jo sabse zyada mahatvapurn hai—ise Albert Einstein ne “World’s 8th Wonder” kaha tha: The Power of Compounding.

Is blog mein hum detail mein samjhenge ki Early Investing Benefits kya hain aur kyun aapko apni 20s vs 30s mein investing shuru karne ka decision dhyan se lena chahiye.

1. What is Compounding in Mutual Funds?

Compounding ka simple matlab hai “paisa par paisa kamana.” Jab aap Long Term Investment karte hain, toh aapko interest par bhi interest milta hai. Shuruat mein growth dhimi lagti hai, lekin 20 saal baad ye ek snowball effect ban jata hai jo aapke Retirement Planning ko aasaan bana deta hai.

The Ultimate Guide:8th Wonder Compounding in mutual fund – Magic Rule of 72

Compounding ko samajhne ka sabse aasaan tarika hai Rule of 72. Ye ek mathematical shortcut hai jo har investor ko pata hona chahiye.

Ye kaise kaam karta hai?

Aapko bas 72 ko apne expected annual return (CAGR) se divide karna hai. Jo number aayega, utne saalon mein aapka paisa double ho jayega.

- Scenario A (Fixed Deposit): Agar aap FD mein paisa rakhte hain jahan 6% return mil raha hai, toh $72 / 6 = 12$ saal lagenge paisa double hone mein.

- Scenario B (Mutual Funds): Agar aap Equity Mutual Funds mein invest karte hain jahan average 12% return milta hai, toh $72 / 12 = 6$ saal mein aapka paisa double ho jayega.

Aditya’s Insight: 20s mein shuru karne ka fayda ye hai ki aap apne paise ko 5 se 6 baar double hote huye dekh sakte hain, jabki 30s mein shuru karne par shayad 2 ya 3 baar hi aisa ho paye.

2. The power of Compounding secrets investing in 20s vs. 30s Magic of Starting Early: SIP Benefits

SIP (Systematic Investment Plan) ka sabse bada fayda tab milta hai jab aap market ko ‘Time’ dete hain. Agar aap 20s mein hain, toh aapke paas sabse bada asset hai—Waqt.

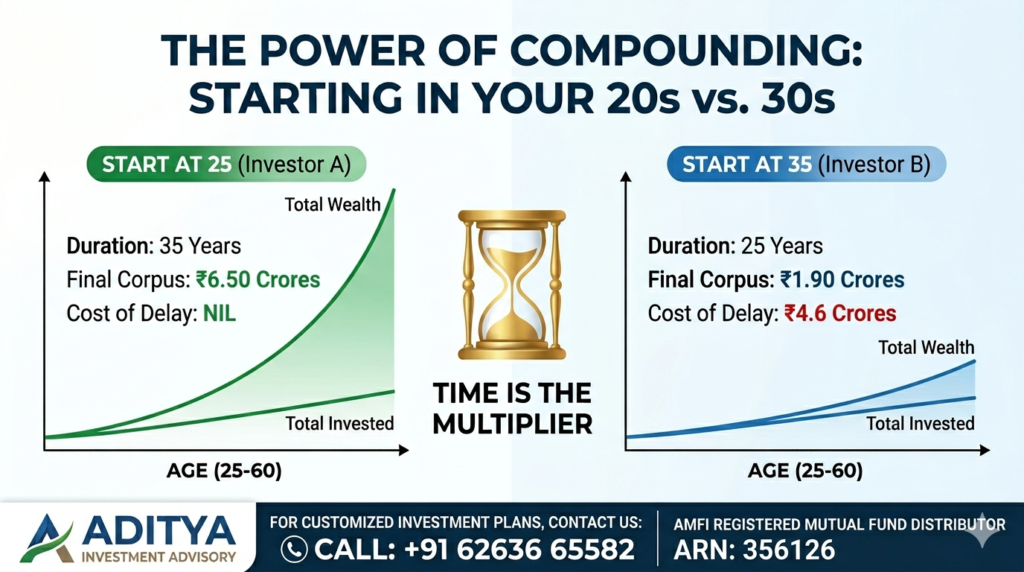

Case Study: Investor A (25) vs. Investor B (35)

Chaliye dekhte hain ki Early Investing kaise crores ka farq paida karti hai:

| Particulars | Investor A (Starts at 25) | Investor B (Starts at 35) |

| Monthly SIP Amount | ₹10,000 | ₹10,000 |

| Investment Period | 35 Years | 25 Years |

| Expected Return (pa) | 12% | 12% |

| Total Wealth Created | ₹6.50 Crores | ₹1.90 Crores |

Conclusion: Sirf 10 saal ka delay karne se Investor B ko lagbhag ₹4.6 Crore ka nuksan hua. Yahi hai power of compounding ka asli chehra.

Step-Up SIP – Amazing Wealth Creation ki Raftar Badhayein

Zyadatar log ye galti karte hain ki wo ₹5,000 ki SIP shuru toh karte hain, lekin 10 saal tak us amount ko badhate nahi hain. Compounding ka asli jadu tab dikhta hai jab aap Step-up SIP ka istemal karte hain.

Jaise-jaise aapki income badhti hai, aapko apni SIP bhi har saal kam se kam 10% badhani chahiye.

- Normal SIP: ₹10,000 per month for 20 years = Approx ₹1 Crore.

- Step-up SIP (10% Annual Increase): ₹10,000 per month with 10% hike every year = Approx ₹2.2 Crores.

Sirf thoda sa extra discipline aapke corpus ko double se zyada kar sakta hai. Ise “Automatic Wealth Multiplier” bhi kaha jata hai.

3. Why Investing in your 20s is a Game Changer

Aapki 20s ki umar Equity Investment ke liye “Golden Age” hai:

- High Risk Appetite: Kam zimmedariyon ki wajah se aap Small Cap aur Mid Cap Mutual Funds mein invest karke zyada returns generate kar sakte hain.

- Discipline for Financial Freedom: Kam age mein invest karne se saving ki aadat padti hai jo life-long kaam aati hai.

- Beating Inflation: Long term mein equity hi ek aisa asset class hai jo inflation (mehangai) ko beat karke real returns deta hai.

Inflation (Mehangai) – Investor ka sabse bada dushman

Blog mein ye point dalna bahut zaroori hai kyunki log sirf “Crores” dekhte hain, uski “Value” nahi. Agar aaj ek ghar 1 crore ka hai, toh 6% inflation ke hisaab se 20 saal baad waisa hi ghar kharidne ke liye aapko ₹3.2 crore chahiye honge.

Compounding vs. Inflation: Agar aapka investment compounding se 12% grow kar raha hai aur inflation 6% hai, toh aapka “Real Return” sirf 6% hi hai. Isliye, 20s mein hi Equity jaise high-growth assets mein invest karna chahiye, kyunki Savings Account ya FD ka return aksar inflation se bhi kam hota hai, jiska matlab hai ki aapka paisa badh nahi raha, balki uski value ghat rahi hai.

4. Better Late Than Never: Investing in your 30s

Agar aap 30s mein hain, toh niraash na hon. Aap abhi bhi ek mazboot corpus bana sakte hain, lekin aapko apni strategy badalni hogi:

- Increase your Investment: Aapko Investor A ke barabar pahunchne ke liye apni SIP amount ko double ya triple karna hoga.

- Step-up SIP Strategy: Har saal apni investment ko 10-15% badhayein taaki compounding ki speed tez ho sake.

- Goal-Based Planning: Apne bachon ki education aur apne Retirement Fund ke liye alag-alag portfolios banayein.

5. The Cost of Delaying: A Heavy Penalty

Financial experts ke mutabik, har ek mahina jo aap bina invest kiye nikalte hain, wo aapke future corpus se lakho rupaye kam kar raha hai. Long Term Wealth Creation ke liye “Perfect Time” ka wait na karein, balki aaj se hi shuru karein.

Psychology of Investing – Log Fail Kyun Hote Hain?

Compounding ka magic isliye kaam nahi karta kyunki log patience kho dete hain. Iske piche 3 bade kaaran hain:

- The Boring Middle: Investment ke shuruati 5-7 saal bahut boring hote hain kyunki returns kam dikhte hain. Log bore hokar investment band kar dete hain.

- Market Panic: Jab share market girta hai, toh log darr kar apni SIP rok dete hain. Yaad rakhiye, compounding tabhi kaam karti hai jab “Uninterrupted Time” mile.

- Lifestyle Creep: Jaise hi salary badhti hai, log naya iPhone ya car EMI par le lete hain. Wo compounding ko apne liye nahi, balki banks ke liye (Interest bharkat) kaam par laga dete hain.

6. Conclusion

Compounding ek race nahi hai, balki patience ka game hai. Chahe aap 20s mein ho ya 30s mein, SIP Benefits tabhi milenge jab aap consistent rahenge. Sahi Financial Planning aur Mutual Fund Investment ke saath aap apne har financial goal ko hasil kar sakte hain.

Frequently Asked Questions (FAQs)

1. Compounding ka pura fayda lene ke liye minimum kitne saal invest karna chahiye? Compounding ka asar 10-15 saal ke baad tezi se dikhna shuru hota hai. Isliye, agar aap 20 saal ya usse zyada ka samay lekar chalte hain, toh aapka chhota sa investment bhi ek bada corpus ban sakta hai.

2. Kya 30 ki umar ke baad shuru karna bahut deri hai? Nahi, der kabhi nahi hoti! Halanki 20s mein shuru karna behtar hai, lekin 30s mein aap apni investment amount (SIP) badha kar aur “Step-up SIP” ka istemal karke apne retirement goals ko abhi bhi hasil kar sakte hain.

3. Agar main beech mein SIP rok doon toh kya compounding par asar padega? Haan, compounding “uninterrupted time” par chalti hai. Agar aap beech mein withdraw karte hain ya SIP rokte hain, toh compounding ka cycle toot jata hai aur aapko naye sire se shuru karna padta hai.

4. Compounding sirf Mutual Funds mein hi hoti hai? Compounding har us jagah hoti hai jahan aapko interest par interest mile. Lekin, Mutual Funds aur Equity mein returns inflation se zyada milne ke chances hote hain, isliye wealth creation ke liye ise sabse behtar mana jata hai.

5. Market girne par mujhe kya karna chahiye? Jab market niche ho, tab aapko apni SIP continue rakhni chahiye. Isse aapko zyada “Units” milti hain (Rupee Cost Averaging), jo market recover hone par aapke compounding returns ko kai guna badha deti hain.

Apni Financial Journey Aaj Hi Shuru Karein!

Kya aap bhi apni financial freedom ka plan banana chahte hain? Compounding ka jadu tabhi kaam karta hai jab aap sahi samay par aur sahi jagah invest karte hain.

Main hoon Aditya, ek certified Mutual Fund Distributor (MFD). Main aapki madad kar sakta hoon ek aisa portfolio banane mein jo aapke future goals aur risk appetite ke hisaab se perfect ho.

Mujhse Contact Karein:

- Website: investmentwithaditya.com

- Services: Mutual Fund Investment, SIP Planning, Retirement Solutions.

- AMFI Registered Mutual Fund Distributor

- ARN Number: [ ARN-356126]

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully. The calculations and examples shown in this blog are for educational and illustrative purposes only and do not guarantee future returns. The actual returns may vary based on market performance. This content does not constitute professional investment advice; please consult with a certified financial expert before making any investment decisions.

Aditya Investment Advisory AMFI Registered Mutual Fund Distributor | ARN: 356126

Leave a Reply